The economy is grim. So why leave money on the table?

The OC&C/WRAP report Are UK Businesses Leaving Money on the Table? quantifies the in-life value most hardware brands currently let walk out the door. Bicycles are the lens I’m looking through but the argument runs right across hardware.

TL;DR

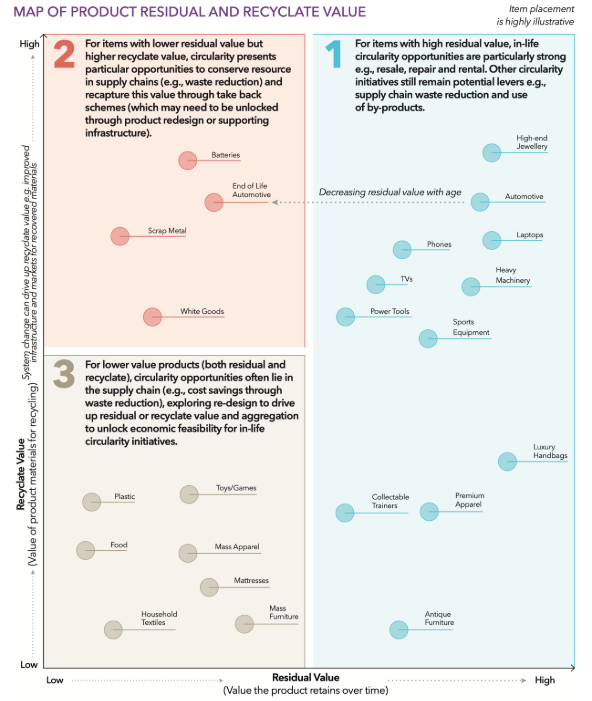

The report places every hardware category on a map of residual value (worth to the next user) and recyclate value (worth to recycling). Where your product sits dictates which circular plays will actually pay.

Bicycles sit top-right — durable, repairable, with mature second-hand and repair markets. Most cycling brands capture only first-sale revenue from a product clearly built to keep paying for many years. Adjacent categories sit in much the same position.

The integration of electronics into mechanical products is quietly walking back that residual-value advantage. E-bikes are the most acute version. Cordless tools, smart appliances, EVs and connected white goods all sit on the same trajectory.

The brand → distributor → dealer model is a blind spot in the report. If your finance team books revenue at dispatch from the warehouse rather than at the user (a nasty bicycle industry trait), you have no relationship with the product’s actual life…and no chance of tapping into the revenue opportunities that live there.

The brands the report holds up — Currys, Apple, IKEA, Patagonia, Bike Club — share one thing: a direct, persistent relationship with the end user. No void.

The question isn’t whether your category will go circular. It’s whether your brand captures the value or watches a third-party aggregator do it for you.

WRAP and OC&C published Are UK Businesses Leaving Money on the Table? in mid-April. A couple of weeks later our DSfEC cohort had an expert session with one of its contributors — Jennifer Emerton, WRAP’s Head of Business Engagement.

The report’s argument is straightforward, if uncomfortable. The circular economy isn’t an environmental ambition slowly hardening into a regulatory threat. It’s a commercial shift that’s already redistributing value, and most hardware brands are on the losing side of it.

Three things in the report are worth pulling out. Bicycles are the worked example, because that’s where I’ve spent most of my career — but the patterns hold across most hardware.

1. Where your product sits decides which circular plays will pay

The report’s most useful tool — for me, at least — is its Map of Product Residual & Recyclate Value.

On one axis: how much value a product retains after first sale. On the other: how much value its materials are worth at recycling. Where a product sits on that map determines which circular plays will actually wash commercially — repair, resale, refurb, rental, PaaS, take-back, or just recovery for recyclate.

The map is striking. Cars, premium apparel, branded consumer electronics and bicycles cluster in the top-right: high residual, decent recyclate, with credible repair and resale economies already gaining traction. Mass apparel, mattresses and bulk household textiles sit bottom-left, where the only viable circular plays are upstream — design changes and supply-chain waste reduction.

Bicycles sit firmly in the top-right. The report lists bikes as mature for repair (level with cars) and gaining traction for both B2C refurb-and-resale and rental/PaaS — citing Bike Club’s £4.49-a-month children’s subscription (55k members across the UK and Germany) as the headline case study.[¹]

In other words: every commercial circularity model the report describes already works for bikes.

The infrastructure exists.

The unit economics work.

And yet most brands in the sector still capture only first-sale revenue from a product clearly built to keep paying for multiple years…

That gap is what the rest of the report unpacks. The shape of the opportunity changes by category, but the question doesn’t:

…of the in-life revenue your product makes possible, how much is going to you, and how much is going to someone else?

2. Integration is killing residual value across hardware

There’s a trend the data quietly reflects, even where the report doesn’t name it. The integration of electronics into products that used to be mechanical is making in-life capture harder at the exact moment in-life capture is becoming the value driver.

In cycling, the most visible version of this is the e-bike. A steel-framed mechanical bike is a refurbisher’s dream. Serviceable indefinitely, parts largely interchangeable across brands and decades, and the second hand market understands the materials.

A mid-drive ebike with a proprietary battery pack, a brand-locked motor controller, and firmware that won’t talk to a third-party diagnostic tool is a very different proposition.

The report places batteries in the high recyclate value zone (i.e. material worth recovering from a financial POV) but also flags them, alongside electronics and tools, as a category “relying on constrained inputs, where access to materials is becoming a strategic concern.”[²]

The pattern repeats across the rest of hardware. Cordless tools that were once dumb mechanical units now carry sealed battery packs. Kitchen appliances ship with apps and cloud accounts. Cars are becoming rolling firmware deployments. Each step toward integration sells more units in the short term and walks back the residual-value advantage in the longer one.

On our current trajectory, our continued strive towards a data rich system is making our products increasingly finite with regards to their usable life span…

This is also where the DPP argument gets sharper. The report names product passports directly as one of the key technologies that unlocks circularity at scale, alongside AI/ML for grading and valuing second-hand items, robotic sorting, and reverse logistics platforms.[³]

Without machine readable provenance on the battery, the motor and the firmware, a second-life market for connected hardware cannot scale. With it, you get the basis for the kind of full-stack third party enabler the report points at (the Foxways and ACS Clothings of the world) handling diagnostics, grading, refurb and warranty as a service.

AFAIK, there is no Foxway for e-bikes yet.

But there will be.

The only question is who builds it, and whose data feeds it.

3. The dealer-model blind spot

The report’s most under acknowledged finding isn’t on the map at all. It’s structural.

A lot of hardware brands — cycling especially, but white goods, power tools, kitchen appliances and consumer electronics too — still operate through a traditional brand → distributor → dealer model.

In some of these businesses, a unit is internally counted as sold at the moment it leaves the warehouse for a distributor or dealer.

Not when an end user unboxes it.

Not when they first switch it on.

Actually, regardless of whether a user chooses to purchase the item at all…

That accounting convention is a leftover from a linear economy where the product-customer relationship genuinely did end at the wholesaler’s loading bay. In a circular economy, it’s a structural blind spot.

Every value driver the WRAP report identifies in its in-life section (additional customer touchpoints, longer product lifetime value, repair revenue, refurb margin, brand loyalty, the data feedback loop that powers everything from forecasting to grading) depends on the manufacturer actually knowing who their users are, what condition their products are in, and when they’re ready for a service, a swap, or a second life.

If your last data point on a given unit is the dispatch note from your warehouse, you are flying blind through exactly the part of the lifecycle where the new value sits…

Compare that to the models the report holds up: Bike Club, Swapfiets, Apple’s certified refurb programme (which recovers c.85% of RRP versus c.70% achieved by third-party refurbishers).[⁴] They all share one thing: a direct, persistent relationship with the end user, often underwritten by ownership or subscription. No void. No layer of intermediation between the brand and the product’s actual use.

A few years ago I led the engineering work on integrating findings from Islabikes’ Imagine Project into the core business, an incubator initiative asking whether a children’s bicycle could be designed to last 50 years and delivered via subscription, so the same bike could pass through multiple riders. We built the data acquisition, FEA validation, in-house lab testing and NDT strategy that a returns grading system needs. None of it would have worked through a traditional wholesale channel that closed the books on bike number one the day it left the loading bay. The channel and the circular product strategy were entangled from day one.

For any brand operating through traditional distribution, the implication is that the channel itself becomes part of the redesign work. Either the model has to evolve (direct-to-consumer, take-back, subscription, certified partner networks with shared data) or the dealer ceases to be an intermediary at all and becomes a co-owner of the in-life relationship: a properly equipped repair, diagnostics and refurb partner, with the data pipe to match.

The DPP, when it lands in regulation, will force some version of this question regardless. Brands that move ahead of it won’t be the ones scrambling when it does.

What capturing the value actually looks like

The brands the report holds up as case studies for in-life value capture aren’t cycling brands. They’re from the categories that worked through this question first.

Currys, with 1.4 million repairs and 15% of revenue from in-house repair services in FY23/24, used explicitly as a differentiator against pure-play online players who can’t credibly offer it.[⁵]

Apple’s certified refurb programme, capturing 85% of RRP versus the 70% achieved by third-party refurbishers.

IKEA, shipping 532k spare parts in the UK alone in FY23 against a product range explicitly redesigned for repairability.[⁶]

Patagonia, sourcing 94% of its wool, 92% of its nylon and 82% of its cotton through its Worn Wear take-back programme.[⁷] In cycling, Bike Club at 55k subscribers and growing.

The common thread isn’t industry. It’s that each of these brands made three commitments that reinforce each other:

They own (or directly control) the relationship with the end user

They invested in the operational capability to bring product back into a gradable, sellable, repairable state

They redesigned the product to make that economically viable

The repair price threshold in the consumer data is striking. Across categories, consumers said they’d pay c.20% of a product’s original price to repair it rather than replace it.[⁸] If your product retails at £500, that’s implied repair revenue of £100 per replacement deferred. If it retails at £4,000, it’s £800. Multiply by the number of units in your installed base, multiply again by the additional years of service life you can credibly underwrite.

That’s not a marginal number.

For cycling specifically, this is the opportunity sitting in front of every independent bike shop: to evolve from a new sales business that’s structurally losing the volume race into the repair-and-refurb partner that brands and end users both need. Currys has shown what that pivot looks like in consumer electronics. The bike shops that move first will hold that position in cycling. The brands that partner with them properly will hold the in-life value currently flowing through them uncaptured.

When we visited Decathlon at Surrey Quays as part of DSfEC, one figure stuck with me: 25% of their bike sales last year were second-life, and crucially, not just Decathlon’s house brands of bikes. They’ve quietly become a multi-brand second hand bike retailer inside what looks, from the outside, like a new sporting equipment shop.

The OC&C/WRAP data corroborates the trajectory — 20% of UK consumers had bought a bicycle second hand in the last twelve months, ahead of laptops, level with premium clothing.[⁹] Refurbished bicycles retail at around 70% of new RRP in Grade A condition.[¹⁰] To borrow Jennifer’s framing: the Oil Tanker has turned a degree or two…

If your bikes are showing up in pre-owned racks elsewhere, that 70% of RRP is now somebody else’s margin.

The same goes for every other hardware category in motion: white goods on Back Market, tools on eBay, apparel on Vinted.

The question for every brand in the room is whether they want to be the Oil Tanker that turns, the third-party aggregator that scales up to fill the gap, or the brand whose volume quietly flows through someone else’s reseller racks.

Closing thoughts

The numbers in the WRAP report say bikes are one of the best-positioned hardware categories for in-life circularity. The same numbers, read differently, say most of that latent value is currently being captured by someone other than the brand that designed the product. The pattern repeats across hardware: cars, electronics, white goods, premium apparel. Different industries, same shape.

A couple of years ago, at Shift Cycling Culture’s barcamp, I argued that design engineers had a responsibility to move the needle on sustainability even when the company mandate wasn’t there. What’s changed since is that the mandate is now arriving via the back door — through bottom-line value, not virtue.

The WRAP report has the numbers to back it up.

If you’re thinking about how a hardware business (bike-shaped or otherwise) moves from a linear sales model to something more circular without bolting it on as a side-project, we’re ready to help.

Sources:

[¹] OC&C / WRAP, Are Businesses Leaving Money on the Table?, pp. 17, 19. [²] Ibid., p. 28. [³] Ibid., p. 10. [⁴] Ibid., p. 26. [⁵] Ibid., p. 23. [⁶] Ibid., p. 23. [⁷] Ibid., p. 28. [⁸] Ibid., p. 22. [⁹] Ibid., p. 24. [¹⁰] Ibid., p. 25.